This is part one of two-part article. Part II can be found here.

Over the last 20 years I have been on an incredible adventure, a journey which originated in the UK but took in some diverse cultures in distant places, including the US and Japan. I’ve had some fascinating traveling companions and we’ve navigated some unfamiliar, and often challenging, landscapes. Many times, we’ve been tight on resources and had tough battles to fight but there have also been plenty of successes to celebrate along the way.

With two oncology drugs discovered through our partnerships now approved for patients, in some ways it feels like I have already achieved my personal goal. So here, I share with you some of my insights in the hope that they inspire other entrepreneurs as they embark on their journeys of discovery.

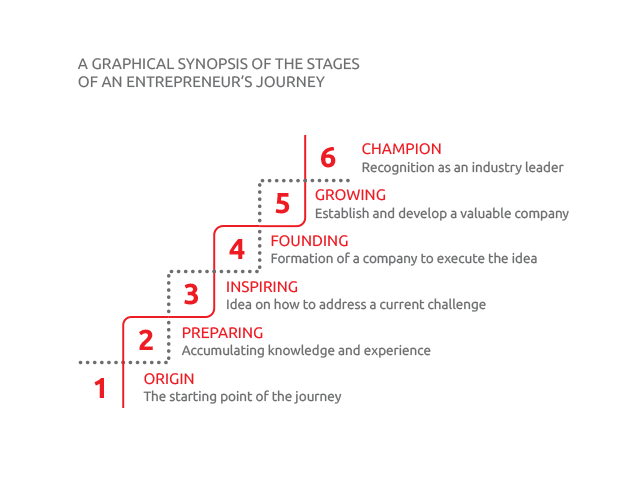

Origin

The journey started in Swindon, a town 70 miles west of London in the UK where I grew up. It was challenging for a British Asian to grow-up in the UK in the 1970s, but those experiences were also rather formative. I attended a local state school where two teachers had a profound impact on me. My chemistry teacher told me I was hopeless at chemistry and that I should never consider a career in science, and the biology teacher told me that Swindon was “the anus of Great Britain” and that I should study hard, pass my exams and get out! I took the latter advice.

Growing up in a working-class British Asian family also gave me some unique insights. I was conscious that we were different, part of a minority, which meant that I was fine-tuned to empathize with others and appreciate different perspectives.

Preparing

Like in most Asian families, education was highly valued, and my parents encouraged me to study hard and follow a professional career that would enable me to be self-sufficient. So, I decided to do a degree in Biochemistry at Queen Mary College, and a PhD in protein crystallography at Birkbeck College, both part of the University of London. The choice of subjects was driven by an interest in biomedical science and, in particular, the emerging area of structure-based drug design.

After my PhD I worked as a post-doctoral scientist at Oxford University, on a collaborative project with the Wellcome laboratories (which later became GlaxoWellcome and then GSK) in which we explored structure-based drug design for a cancer target.

In 1991, I made the leap into the commercial world of ‘big pharma’ by joining Glaxo (which later became GlaxoWellcome then GSK), and over a period of nine years progressed to become Head of Structural Biology and Bioinformatics.

Inspiring

During my time at GlaxoWellcome, it became apparent to me that structural biology could be used in a much more impactful manner in drug discovery. Furthermore, it was a really exciting time, with lots of new biotech companies emerging, especially in the US, to challenge traditional methods of drug discovery and development.

One research area that was particularly inefficient was small molecule lead discovery. During the nineties, significant investment had been made by the industry in combinatorial chemistry and high-throughput screening (HTS), but this had not delivered on its initial promise of increasing the numbers and quality of new drugs entering clinical trials. This was, in part, due to the complexity and relatively large size of the compounds routinely being screened, as well as the challenge of optimizing the hits derived from this approach.

So, in a great surprise to my GlaxoWellcome colleagues, I resigned my safe, secure job and decided to start a biotech with the aim to address this challenge.

Founding

In 1999 I founded Astex Technology Ltd in Cambridge with Prof. Sir Tom Blundell and Prof. Christopher Abell, which pioneered the development of “fragment-based drug discovery” as a novel approach to generate small molecule drugs.

Fragment-based drug discovery identifies small chemical fragments, which can be combined or enlarged using structure-guided medicinal chemistry to produce a lead compound with optimal drug-like properties for the biological target. At Astex we called our proprietary fragment-based drug discovery platform Pyramid. Traditional bioassays used in HTS are generally unable to detect such small drug fragments because of their low affinity of binding to the protein target. However, biophysical techniques are ideal to detect low affinity binding events. The Pyramid platform integrates a range of high-throughput biophysical techniques for screening, such as X-ray crystallography, nuclear magnetic resonance spectroscopy, and calorimetry with fragment library design and computational methodologies. More recently, we’ve been integrating cryo-electron microscopy into our platform. Unlike conventional screening techniques, the Pyramid process enables precise details of fragment binding to be routinely identified and visualized, therefore allowing for rational molecule design.

The formation of Astex resulted from multiple discussions with Abingworth, one of Europe’s leading life sciences venture capital companies, which became our founding investor. The initial concept for the company was developed by me and Roberto Solari (ex-Glaxo) who had joined Abingworth and later became a non-executive director representing Abingworth on the Astex Board. The founding investor has a critically important role in the formation of a new biotech. Apart from providing the funding, they also help shape the investor syndicate, propose potential Board members, and provide general advice for the new management team.

As the founding CSO of Astex, one other key job was to identify a CEO who would work with me to build the company. Often founding scientists insist on being CEO, but I’ve always held the view that anyone joining Astex needs to be credible and impactful from day one. I was aware that I did not have the appropriate skills and expertise to perform as a credible CEO at that time. We were fortunate to hire Tim Haines as our first CEO; he was an experienced executive who had a background in finance and had also led medical device companies, so nicely complemented my own big pharma scientific background.

Growing – an eventful journey

There have been three main phases of company growth and development during my Astex journey.

The first was when we were a venture-backed, Cambridge, UK-based company. Once we had built our platform technology, we operated a hybrid business model. We partnered with pharma companies such as AstraZeneca, Novartis, Janssen and GSK, to both validate our technology and generate revenues, whilst also developing our own pipeline of therapeutic candidates. There are pros and cons to this approach, and the Board often had lively debates regarding the best way forward. In the short term, the partnerships brought in much needed cash. However, over the longer term, you need to be careful how much value you give away, and the fine details of the deals that you strike. Also, as we learnt later to our detriment, not all pharma partners are the same in their culture and morals! Nevertheless, at this time in its development, Astex was in the lucky position of having money, options and opportunities. It had also progressed its internal pipeline of compounds to the early stages of clinical development, which triggered the company to be renamed Astex Therapeutics Ltd in 2005. During this first phase, the Astex Board was broadly aligned and supportive, even during the uncertain period after Tim Haines stepped down from the CEO position in 2005. I was appointed CEO in 2007, after the Board had initially hired an external candidate but who turned out not to be an optimal fit.

The second phase of growth and development occurred in 2011, when Astex Therapeutics Limited merged with SuperGen, a California-based, NASDAQ-listed company, to form Astex Pharmaceuticals. The merger came about while Astex was looking to access the public markets in the UK via an IPO, to finance its growing clinical pipeline. However, biotech IPOs in the UK have always been difficult for a non-revenue stage company, so there was strong appeal for a merger with a US publicly listed biotech with a good financial position.

Furthermore, SuperGen had significant expertise in clinical development and regulatory capabilities, which complemented our strong drug discovery engine. The vision was to create a new world class oncology company, to generate a vibrant and growing R&D pipeline, backed by an established revenue stream and a strong capital foundation. It was to be named Astex Pharmaceuticals. The proposed merger was a big challenge for the Astex directors, and triggered significant debate at the Board level, but they eventually accepted that this was a ‘company building event’ rather than an exit. Even so, we had to have two attempts at getting agreement from all Astex Board members, as the first attempt was aborted after one director refused to sign at the eleventh hour. This experience taught me a lot about how a CEO needs to manage a Board; when to cajole and when to threaten to use the ‘nuclear option,’ i.e. resign! We eventually succeeded and became a US-based and NASDAQ listed company in October 2011. During the merger process I stepped down from the CEO position at Astex to take on the role of president, but I retained my board seat in the new company. I was happy taking on this new role as it was clear that the CEO of the new company would need to be in the US, and the SuperGen CEO, Jim Manuso, was US-based and keen to keep his position. I felt I could maintain my influence on the strategic direction of the company at the board level.

At that time, the Board of Astex Pharmaceuticals included five former SuperGen and four former Astex directors, which broadly reflected the share-holding structure of the new company. After an initial honeymoon period it became rapidly apparent that the board was struggling to find consensus and alignment regarding corporate strategy. I experienced several challenging encounters with some board members and, crucially, also the CEO during the subsequent two years. While the company was in a strong financial position, the lack of strategic alignment within senior management and also at the board level prompted a decision to explore a sale of the company. A formal M&A process was initiated to explore possible transactions that could result in generating maximum value for shareholders. The process concluded in 2013, with Astex taking another leap forward when it was acquired for $886m by Otsuka Pharmaceuticals of Japan. This heralded the third and current phase of our growth. This was the seventh largest global life science M&A transaction in 2013 and underlined the value of our programs and platform technology. The acquisition made sense to Astex on a number of levels. Otsuka could provide lots of useful big pharma resources including financial support as well as the potential for us to expand into other therapeutic areas. Otsuka also promised to be hands-off, recognising the need for significant autonomy at Astex to maintain our successful entrepreneurial spirit. Indeed, the insistence by Otsuka that Astex should retain its name and separate identity was symbolic and reinforced the ‘satellite structure’ that Otsuka operates for R&D. Otsuka has continued to provide Astex with strong support, and it is no accident that the vast majority of our staff remained several years after the acquisition, which is not the norm in such situations.

Part II coming....

Follow the Topic

-

Nature Biotechnology

A monthly journal covering the science and business of biotechnology, with new concepts in technology/methodology of relevance to the biological, biomedical, agricultural and environmental sciences.

Please sign in or register for FREE

If you are a registered user on Research Communities by Springer Nature, please sign in

thank you for sharing your great journey - it’s been great to work with you along the way.