Concentration of asset owners exposed to power sector stranded assets may trigger climate policy resistance

Published in Sustainability

What is asset stranding and why does it matter for me?

Reaching the 2°C climate goal requires a fundamental transformation of the energy sector. This involves leaving fossil fuels untapped and retiring fossil fuel-based infrastructure prematurely (known as "asset stranding"). The success of climate policies guiding this transition depends on their interaction with stranded assets: Owners of assets at risk of stranding have been shown to strongly oppose such policies, making it necessary to account for their resistance in policy recommendations. So, if you are a climate policy advocate, continue reading to see who are the potential stakeholders making it so difficult to implement policies to mitigate climate change. If you are a policymaker or policy advisor, this is a must-read anyways.

Okay, so what exactly do we want to know about asset stranding?

To better understand potential sources of climate policies resistance, we want to identify key stakeholders in national and international climate negotiations. Thus, we ask: Who owns stranded assets in the global power sector and how are these assets distributed among them? Further, the study analyzes whether adversely affected asset owners invest in alternative energy assets. This is important as alternative energy assets may benefit from climate policies and therefore reduce asset owners’ policy resistance.

Wait… This has not been done in the literature?

Not exactly. Existing research on power sector asset stranding has primarily examined the global or national perspective, offering valuable insights into the extent and costs of asset stranding. However, there is a lack of information regarding affected stakeholders below the national level, particularly how these costs are distributed among asset owners. Understanding this distribution is essential for anticipating resistance to policies and providing realistic policy recommendations. While a few papers have delved into asset stranding at a more detailed level, they focus on either German companies or the upstream fossil fuel sector. This paper addresses this gap in the literature by globally assessing power sector asset stranding at the asset owner level.

Convinced. Now how are stranded assets calculated?

In this paper, we compute stranded assets in the power sector using a unique approach that combines two datasets. The first dataset, provided by Asset Resolution, covers assets in energy-related sectors, their direct owners, as well as the entire ownership structure. This study focuses on a subset of this data related to the power sector, including details such as power plant operating capacity, age, and location. The Asset Resolution dataset is matched with data from the International Energy Agency's (IEA) World Energy Outlook 2021. The IEA data outlines a scenario for regional fossil fuel power capacities that align with the 2°C climate goal (referred to as the "Sustainable Development Scenario"). If the operating capacity of power plants, as indicated in the Asset Resolution data, exceeds the climate-compatible capacity, as given by the IEA data, the study identifies power plants as stranded. Stranded assets are then calculated as the power plants’ overnight capital costs that will not be recovered due to premature decommissioning.

Enough on the methods. So, where on Earth are those stranded assets located?

The study's findings indicate that stranded power plants are primarily located in the Asia-Pacific, Europe, and the United States. Most stranded plants use coal as energy source. While many regions across the globe have already announced climate pledges, which result in the premature decommissioning of power plants, such pledges are often insufficient for reaching the 2°C climate goal. This study finds that especially in the Asia-Pacific and Europe (outside the European Union) a significant number of additional power plants (mostly coal) need to be stranded to achieve a sustainable development.

Stranded assets across regions (Panel a) and across fossil fuels (Panel b). Region abbreviations in the legend are as follows: United States (US), Russia (RU), North America excluding the US (NAM-US), Middle East (ME), Japan (JP), India (IN), Eurasia excluding Russia (EURASIA-RU), Europe (EUR), Central and South America excluding Brazil (CSAM-BR), China (CN), Brazil (BR), and Asia-Pacific excluding China, India, and Japan (ASIAPAC-CN-IN-JP).

And how are they distributed between asset owners?

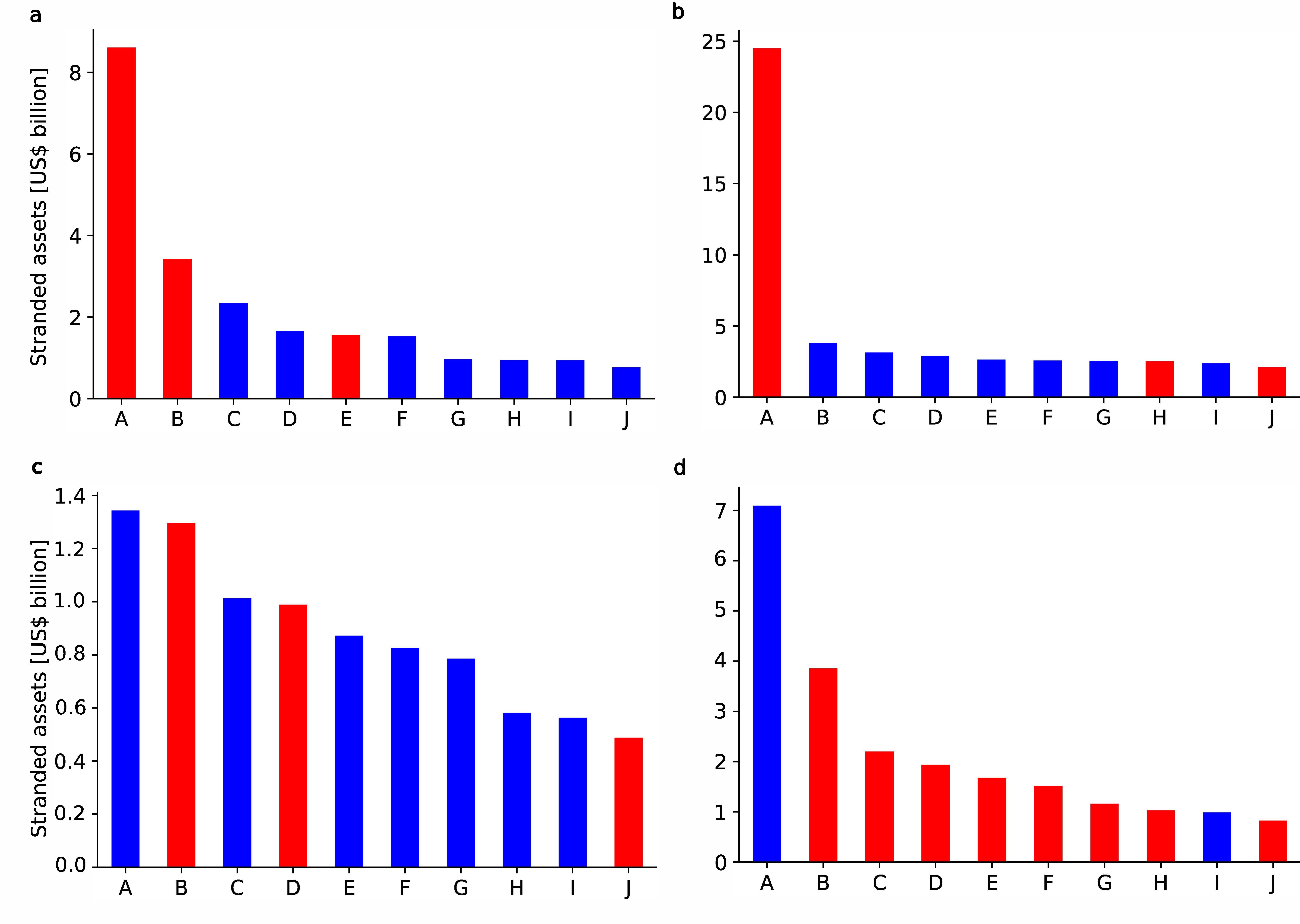

The distribution of stranded assets among asset owners varies significantly in different countries. For example, in India, a single asset owner owns the majority of stranded assets, whereas in the United States, stranded assets are more evenly distributed among asset owners. Coordinating climate policy resistance between these various equally exposed asset owners may be more difficult in the United States compared to India, where stranded assets are concentrated in a single owner. Even if asset owners are equally exposed to stranded assets, the timing of each owner’s asset stranding can differ due to variations in the age profile of power plant fleets.

Each bar represents total stranded assets of a direct owner, which are located in the same country as the direct owner’s headquarter, namely in China (Panel a), India (Panel b), the US (Panel c), and Japan (Panel d). For names of the direct owners represented by capital letters for conciseness, please refer to the supplementary information in the paper.

Do asset owners only own stranded assets located in their own country?

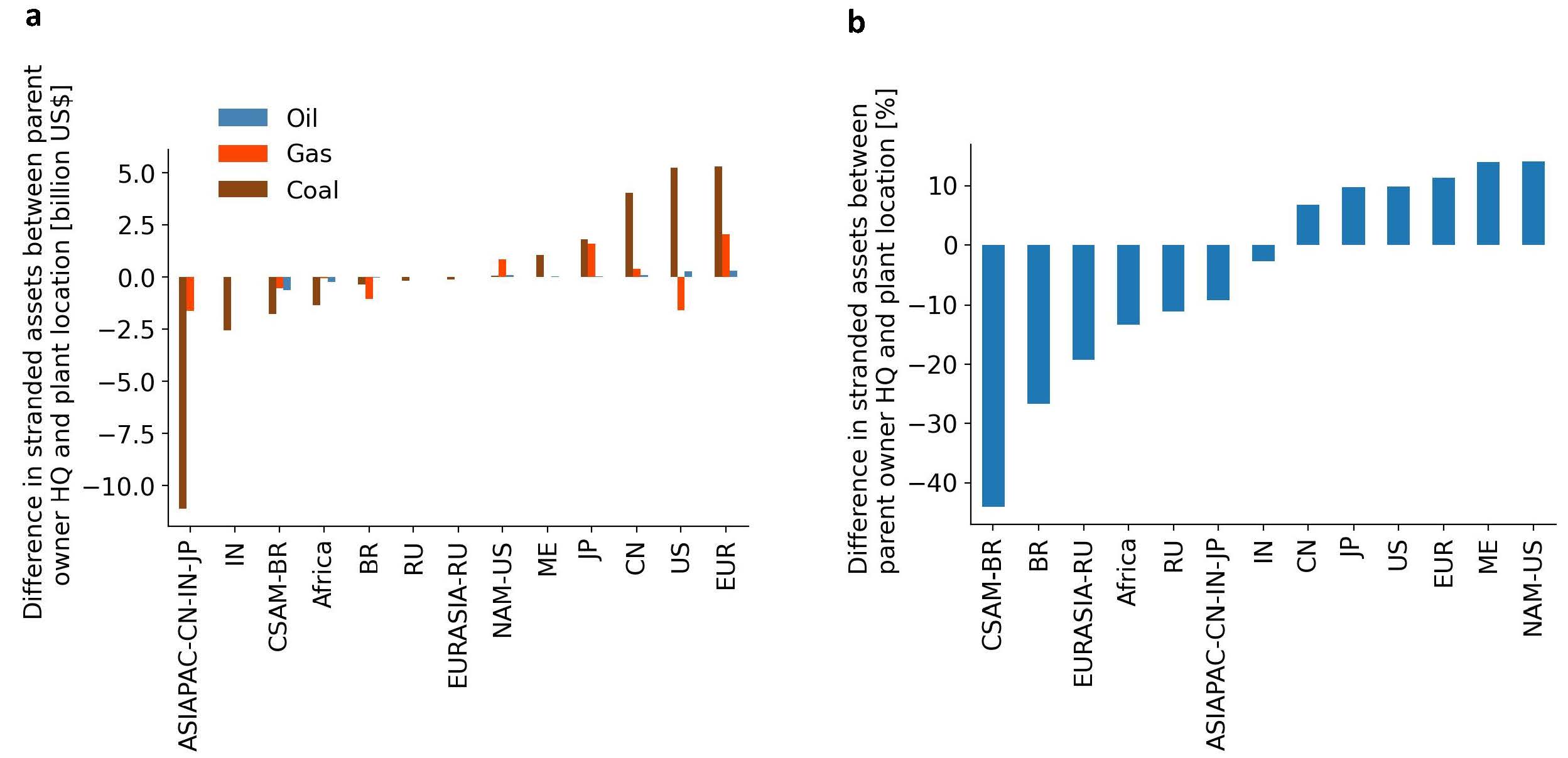

Absolutely not. The location of stranded power plants often differs from the location of the asset owners who ultimately own these plants. European, U.S., and Chinese asset owners own a significant portion of stranded coal power plants in foreign countries. Thus, resistance to climate policies may not only be put up at the national level.

Panel a: Difference in stranded assets between parent owner headquarter and plant location differentiating between fossil fuels. Panel b: Difference in stranded assets between parent owner headquarter and plant location aggregated over fossil fuels. Region abbreviations on the horizontal axis are as described in the first Figure.

What about asset owners listed on stock markets?

Asset owners listed on stock markets may see a substantial portion of their share price (up to 78%) or over 80% of their total equity stranded. This may incentivize listed asset owners to oppose the implementation of climate policies. Listed asset owners in OECD countries show higher levels of equity compared to those in non-OECD countries, which may be crucial for cushioning their asset stranding exposure.

This all sounds pretty dramatic. Can we still end on a positive note?

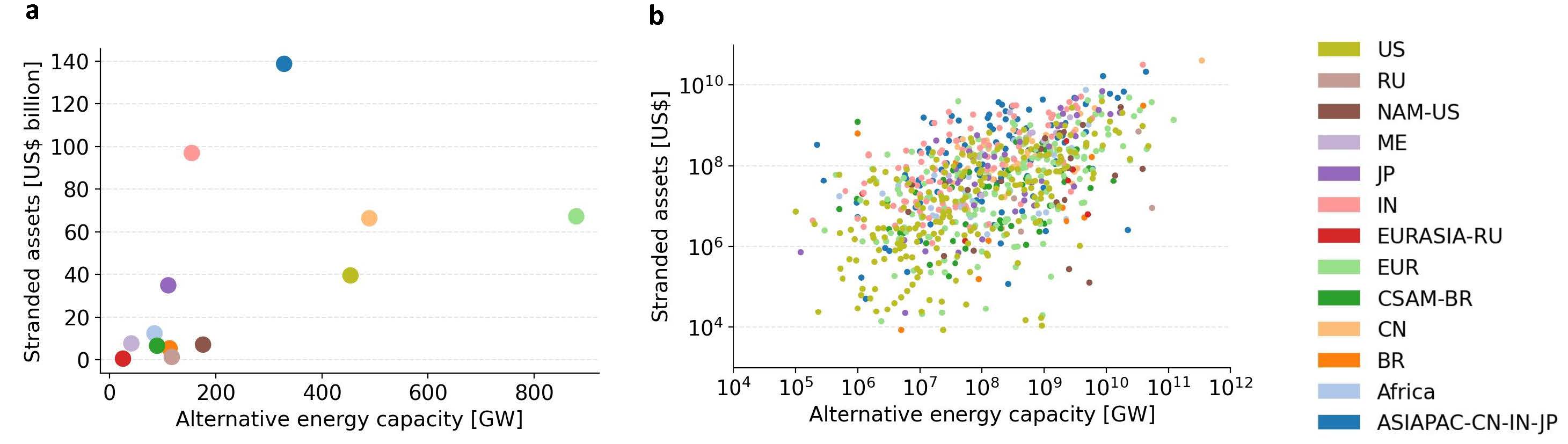

The study also reveals a positive correlation between asset owners' ownership of alternative energy assets and their exposure to asset stranding. China and India, in particular, stand out as highly exposed to asset stranding, with China having relatively more ownership of alternative energy assets compared to India. Investments in alternative energy assets may reduce climate policy resistance.

Panel a: Stranded assets and alternative energy capacity across regions. Panel b: Stranded assets and alternative energy capacity across parent owners. Region abbreviations in the legend are as described in the first Figure.

And why did you say this post a must-read for policymakers and policy advisors?

Policymakers should keep in mind this interaction of climate policies and asset stranding. Stringent climate policies are unlikely to succeed if adversely affected asset owners resist their implementation. As the study shows, asset owners differ significantly in their exposure to prematurely decommissioned power plants. Consequently, resistance to climate policies can vary considerably across dimensions such as owner types, countries, time, and energy source. The design of climate policies needs to carefully address these nitty-gritty details of asset stranding – both, in the power sector and other energy-relevant sectors – to enable the implementation of stringent climate policies required for reaching a sustainable transition towards a low-carbon economy.

Follow the Topic

-

Nature Communications

An open access, multidisciplinary journal dedicated to publishing high-quality research in all areas of the biological, health, physical, chemical and Earth sciences.

What are SDG Topics?

An introduction to Sustainable Development Goals (SDGs) Topics and their role in highlighting sustainable development research.

Continue reading announcementRelated Collections

With Collections, you can get published faster and increase your visibility.

Women's Health

Publishing Model: Hybrid

Deadline: Ongoing

Advances in neurodegenerative diseases

Publishing Model: Hybrid

Deadline: Mar 24, 2026

Please sign in or register for FREE

If you are a registered user on Research Communities by Springer Nature, please sign in