COVID-19, economic policy uncertainty and stock returns in selected European countries: a wavelet analysis

Published in Research Data, Statistics, and Economics

This paper has employed a suite of wavelet techniques to investigate the dynamic relationship between economic policy uncertainty (EPU) and stock market returns in major European economies, with a specific focus on the disruptive impact of the COVID-19 pandemic.

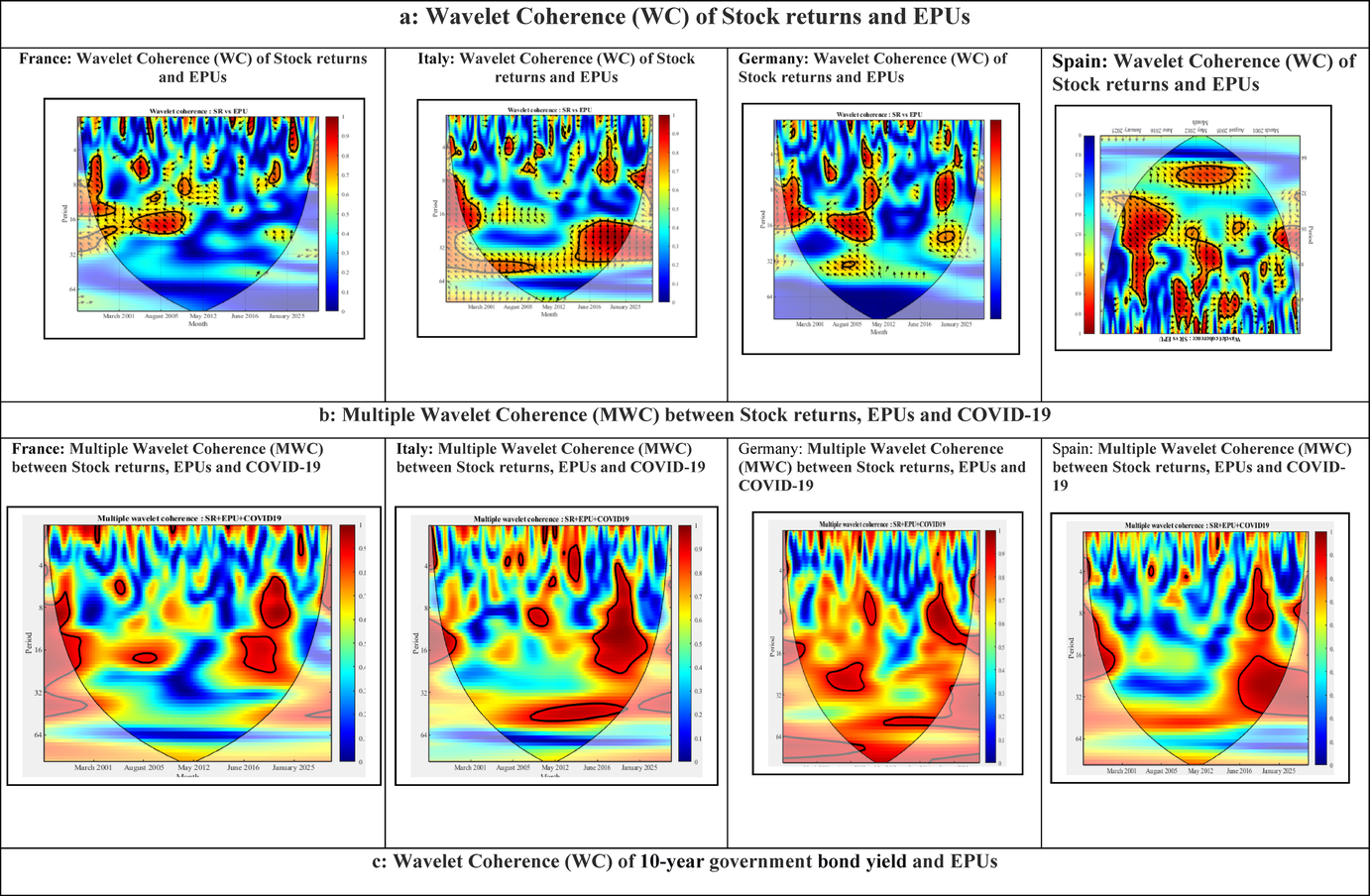

Our analysis yields several pivotal findings that both confirm and extend the existing literature. First, wavelet coherence results confirm a significant and persistent interdependence between stock returns and EPU, particularly within the 4- to 32-month frequency bands. This finding aligns with a substantial body of pre-pandemic research, such as the work of Brogaard and Detzel (2015) and Arouri et al. (2016), which established EPU as a significant predictor of stock market volatility. However, our time-frequency approach refines this understanding by pinpointing the specific medium-term horizons where this relationship is most intense.

The predominant lead of stock returns over EPU, as revealed by phase difference analysis, offers a nuanced perspective. While Pástor and Veronesi (2012, 2013) theorized a strong feedback loop from policy to markets, our results suggest that in the European context, investor sentiment and market performance often serve as leading indicators for subsequent policy uncertainty. This potentially reflects markets anticipating economic downturns that then trigger uncertain policy responses.

The pandemic fundamentally altered this dynamic. Our Multiple Wavelet Coherence analysis demonstrates that COVID-19 acted as a potent catalyst, intensifying and expanding the co-movements between uncertainty and equity markets. This finding resonates with the early observations of Baker et al. (2020) and Goodell (2020), who identified the pandemic as an unprecedented source of market shock. Our paper quantifies this effect, showing it not as a temporary spike but as a structural intensification of the uncertain tyre turn nexus across multiple time scales.

A critical nuance emerges from our Partial Wavelet Coherence analysis. After controlling for Germany’s EPU, the direct relationship between other countries’ stock returns and their own EPU or the COVID-19 shock diminishes significantly. This indicates that the contagion of uncertainty during this period was heavily channeled through spillover effects from the core European economy. This finding provides a crucial empirical underpinning for the survey-based concerns of institutions like the World Economic Forum (2020) and aligns with the concept of a ‘Germany-centric’ financial sphere in Europe. It suggests that the impact of local policy uncertainty in peripheral nations can be overwhelmed by uncertainty shocks emanating from the regional core.

These results offer clear implications. For investors, the consistent behavior of economic agents across different markets and the dominant spillover effect from Germany highlight the critical need to monitor leading uncertainty indicators in systemically important economies, rather than focusing solely on domestic conditions. For policymakers, particularly within influential nations like Germany, our findings emphasize that domestic policy stability is not merely a national concern but a regional public good, as clear and predictable policy directly contributes to insulating neighboring equity markets from volatility.

Methodologically, this paper underscores the value of wavelet analysis in disentangling complex time-frequency relationships in finance. Future research could build upon this foundation by employing more advanced transforms, such as the Dual-Tree Complex Wavelet Transform, to overcome limitations like a lack of shift-invariance. Furthermore, applying this framework to other regional blocs or incorporating additional asset classes could provide a broader understanding of global uncertainty spillovers.

Follow the Topic

-

Empirica

This is a journal that publishes high-quality empirical research from all fields in economics with a particular focus on European economies.

Please sign in or register for FREE

If you are a registered user on Research Communities by Springer Nature, please sign in