Biomedical Innovation in Brazil: an update

Published in Bioengineering & Biotechnology

In our 2018 post [1], human health digital technologies and molecular diagnostics were described as the major drivers of biomedical innovation in the country. Diagnostic companies and private research hospitals were considered protagonists of a complex ecosystem. Since Covid-19, health providers and stakeholders of the biomedical ecosystem had to adapt to a new reality: digital business became mandatory.

The urgent need for digital transformation allowed no time for prejudices or bureaucratic sagas and accelerated the pace of badly needed institutional changes. Telemedicine, remote work, collaborations, it all had to work.

The health care sector in Brazil, considered one of the most fragmented in the world[2], is going through a consolidation process. This process started in 2015, with regulatory changes that allowed foreign investments in the health sector of the country. While there were five merger and acquisitions (hospital deals) in 2015, we saw 32 M&As happening in 2021[3]. If clinical laboratories are considered, the number jumps to 137 M&As[4].

The diagnostic companies and private hospitals, thought of as probable outputs of innovation, now have leading roles in integrating different segments of the health care market. In order to achieve this, they have relied on startups, which proliferated greatly in the past few years and have enjoyed an unprecedented amount of angel and seed capital. In the midst of several ongoing developments, the text below offers a glimpse of this fast-moving landscape.

Integrating health care

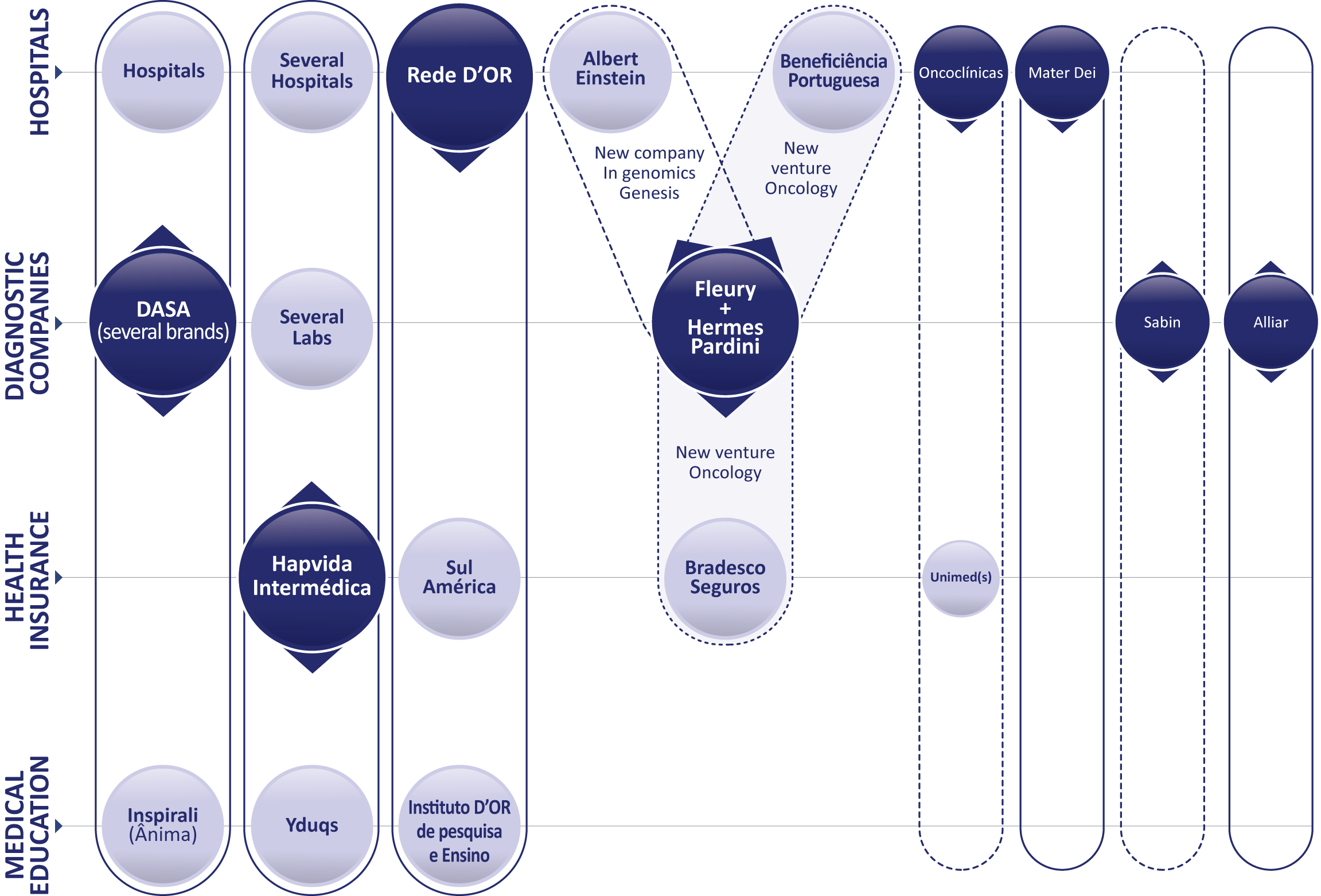

Approximately three years ago, DASA, the biggest diagnostic company in Brazil, made the first move towards integrating health care by investing in the acquisition of hospitals. It became the second biggest hospital group, behind Rede D’Or. DASA’s main competitor in the diagnostic field, Fleury, recently merged with Hermes Pardini, another giant in diagnostics. The merger brought Fleury-Hermes Pardini revenues closer to its rival[5]. Also, in the course of integrating medical care, Fleury has acquired (and still is) medical clinics. Figure 1 indicates two additional institutions that are often in the headlines as leaders of the consolidation process, Rede D’Or and the Hapvida-Intermédica group. The merger of Hapvida and Intermédica group was completed in the beginning of 2022 and just some months later, SulAmérica, their competitor in the insurance segment, was bought by Rede D’Or.

Figure 1) Main events and players in the consolidation process of the health care market in Brazil. Horizontal lines represent the different segments: hospitals, diagnostic companies, health insurance and medical education. Vertical silos represent the verticalization process by the biggest leading institutions (bigger circles in darker shades of blue): DASA, Hapvida/Intermédica group, Rede D’Or, Fleury-Hermes Pardini. Smaller circles in darker shades of blue represent other smaller-sized important players, also involved in acquisitions, innovation and establishment of partnerships. Full lines imply integration mostly through acquisitions and segmented lines integration through partnerships (non excludent).

Another segment that is part of the verticalization process is medical education. In itself, a lucrative business. Apparently, the bigger the better is not only good to make hospitals, diagnostic and insurance companies more profitable, but also applies to private education. Inspirali, the health arm of the group Ânima, was acquired by DASA, Yduqs by Hapvida-Intermédica.

Other relevant examples as provided in Figure 1: Oncoclínicas, a divestee from Fir Capital[6] and the hospital Mater Dei, both are among the five biggest hospital groups[7]. In addition, the figure shows two other diagnostic laboratories, Sabin and Alliar. It is worthy of note that both genomics and oncology are areas of intense competition among the leading consolidators (figure 1). Areas that are also drivers for joint ventures. In partnership with the Albert Einstein Hospital, Fleury is creating a new genomics company, to be called Genesis. The goal is to group the initiatives of both institutions (Fleury and Albert Einstein Hospital) in one genomics company. In oncology, Fleury is establishing a partnership for a new company with the hospital Beneficiência Portuguesa and the insurance company Bradesco Seguros (which is one of Fleury’s major shareholder). The group Oncoclínicas, specialized in oncology, established partnerships with different Unimeds (which are medical cooperatives that offer insurances).

In terms of therapeutic priority, oncology is the focus for the institutions represented in figure 1. Only time will tell how these integrated health systems will conciliate prioritizing a preventative approach to care with the fact that a great part of their revenues will probably come from treating cancer patients in their own hospitals.

Genomics is an extremely important business for all the diagnostic companies and hospitals, it is an expanding market. It only represents 1% of the total market of diagnostic tests, estimated at R$25 B in 2022. By considering that in the US this percentage can be of 10-20% of the total tests, the assumption is that the opportunity for growth is ripe. In fact, both Fleury and DASA have reported a two-digit consistent annual growth rate since 2017[8].

Super-sizing may lead to more profits but the stakeholders promise is that it will also provide better and less expensive care for the patient. By prioritizing prevention and integrating data from genomics and digital platforms, the service-provider will command tools to offer a holistic and more personalized care for the patient. In other words, make a better journey for the patient while keeping health care more sustainable. This sounds excellent and is repeated almost like a mantra by many. Is it possible? According to some of our interviewees[9], there is room for optimism.

For example, DASA’s digital platform, NAV, which has had 23 million users in one year, tracks exams, supports interoperability (one can import exams from a different service provider) and informs doctors if some action is needed. The average time from diagnostic to treatment of breast cancer patients was reduced from 60-90 days (the national average of the private sector) to 12-13 days[10].

To scale up efficiently, the support of digital technologies and several layers of artificial intelligence are crucial and this is where the startups and innovation hubs come in.

Innovation hubs and startups

It is difficult to keep track of all that is going on in the Brazilian health market, but there are initiatives doing a good job at gathering and organizing information[11]. Distrito is one of them. It manages innovation hubs and the latest created, for healthtechs, is inside Hospital das Clínicas at USP University, InovaHC. Their HealthTech Report points to more than a thousand startups in the country[12]. A number also published by a study made by Sling hub for Valor Econômico[13].

According to ABStartups and Delloite Brasil, 45% of the heathtechs were founded in the years of 2019-2021 and only 14% have not received investment[14]. In 2021, USD 530 M were invested in these startups, an increase of 402% relative to 2020[15].

|

Table 1-Innovation hubs launched since 2018 |

|

|

Name |

Website |

|

Albert Einstein Hospital/Biotechnology Innovation Program |

https://www.einstein.br/ |

|

Distrito InovaHC |

https://distrito.me/ |

|

Learning Village |

https://learningvillage.com.br/ |

|

LifeHub SP |

https://www.bayer.com.br/pt/lifehub-sp |

|

Plug and Play Brazil |

https://www.plugandplaytechcenter.com/events/brazil-launch/ |

|

Skyhub |

https://www.skyhub.bio/ |

|

State |

https://www.state.is/ |

|

The Green Hub |

https://thegreenhub.com.br/ |

|

Vibee |

https://www.vibeeunimed.com.br/ |

Table 1 shows some innovation hubs dedicated to health care technologies created in the past few years. Most of them are accelerators, some have their own investment funds. They provide connections with investors, mentors and international hubs. Corporate venture is also on the rise. The laboratory Sabin (show in figure 1) launched Skyhub, its accelerator/incubator and a venture capital fund, Kortex, in partnership with Fleury. DASA, Fleury, Rede D’Or have their corporate funds, so do the national pharmaceutical companies.

What kind of innovation is being developed by these healthtechs? Most technologies aim at management solutions, electronic health records, access, telemedicine and market place [14, 15]. It all looks like the innovation ecosystem is serving healthcare systems for local service delivery. According to one of the interviewees, we had a stage in which there was a disconnection between the solutions being offered by startups and the problems that had to be solved, this is no longer the case, there is a good virtuous cycle now, but it seems to me that everyone is doing a bit of the same.

Final remarks: how about biotechnology?

Accelerators and programs have proliferated, so did international connections and venture builders. Startups have a stronger environment to flourish, they can enjoy several programs to accelerate their business. In addition, entrepreneurs can find specialized mentorship and will probably be able to find angel investors or seed capital.

As mentioned before, the health system in Brazil is highly fragmented and there is still plenty of room to create, expand, and make services more efficient. Nevertheless, a biomedical innovation ecosystem needs enterprises that are outputs of innovation, developers of proprietary technology. From our own research, of the institutions represented in figure 1, only the Albert Einstein Hospital has had a significant number of patents filed in the last decade. The interviews conducted indicate that a strategic approach to proprietary technology does not seem to be a priority. According to the report written by ABStartups and Delloite, only 16.9 % of all startups have patents.

What happens with the entrepreneurs that want to develop a novel solution for cancer care, for instance? Or to develop a new drug against Alzheimer? They will still have a very arid time, as they need the sort of investment that is either non existent or very hard to come by. In addition, these projects are riskier and require more time to market, not the sort of thing most of the investors here have appetite for, specially, if they have other options. Nevertheless, despite the odds, more of these projects are being created.

We have some interesting examples. Scirama, company dedicated to therapeutics based on psychedelic substances; miRScience, which is developing microRNA-based therapies for metabolic like non-alcoholic fatty liver disease, muscle atrophy and cancer; ImunoTera, developing a new immunotherapy for cancer; Celluris, focused on CAR-T cells, FUTR BIO, created to explore a new generation of mRNA vaccines. This latter, is an investee of Vesper Ventures, a venture builder initiative located in the State of Santa Catarina, south region of Brazil. Santa Catarina has a very successful innovation ecosystem. Vesper Ventures launched a biotechnology-focused venture fund and already has a portfolio of companies[16].

The Albert Einstein hospital in São Paulo is a protagonist of biomedical innovation. Its new endeavor, the program to innovate in biotechnologies, will hopefully follow the success of its incubator/accelerator Eretz Bio. The new program aims at stimulating the creation of new businesses in drug discovery and novel treatments, it is close to the hospital, the researchers and clinical trials.

The new extraordinary building that hosts the program, is a teaching, research and innovation building, home to medical students, laboratories, clean rooms for cell and gene therapies. The director of the Center for Research in Immuno-oncology (CRIO), Kenneth Gollob, recently moved to Albert Einstein with his research team from the A.C.Camargo Cancer Center (Figure 2). With a grant of more than R$ 20 million, CRIO was formed via the FAPESP Centers for Research in Engineering (CPE) program in partnership with the pharmaceutical company GSK. He is extremely happy with the new home, the funding and the future to come. Who wouldn’t be?

Figure 2) Researcher Kenneth Gollob and team at the Albert Einstein Hospital’s new teaching building.

[1] https://bioengineeringcommunity.nature.com/posts/40607-breaking-through-asphalt, access on 26.09.2022.

[2] Interview with DASA executive. According to Valor Econômico, there are 1.86 thousand private hospitals, 697 health insurance companies and thousands of laboratories spread throughout the country https://valor.globo.com/empresas/noticia/2022/06/30/movimento-acelerado-rumo-as-compras.ghtml

[3] https://valor.globo.com/publicacoes/suplementos/noticia/2022/05/31/mercado-em-ebulicao.ghtml, access on 26.09.2022.

[4] https://valor.globo.com/publicacoes/suplementos/noticia/2022/04/07/hora-da-integracao.ghtml, access on 26.09.2022.

[5] Pending approval by CADE (Conselho Administrativo de Defesa Econômica). https://valor.globo.com/empresas/noticia/2022/06/30/fleury-e-pardini-companhia-combinada-tm-receita-de-r-61-bilhes-prximo-da-lder-do-setor.ghtml, access on 26.09.2022.

[6] Fir Capital http://www.fircapital.com/

[7] https://valor.globo.com/publicacoes/suplementos/noticia/2022/05/31/mercado-em-ebulicao.ghtml, access on 26.09.2022.

[8] Fleury investor’s day 2021, available at https://ri.fleury.com.br/ and personal communication.

[9] Our many thanks to Luiz Fernando Reis (Hospital Sírio-Libanês, Kenneth Gollob (Albert Einstein Hospital), José Eduardo Levi, Sérgio Ricardo Santos and Heron Werner (DASA), Gustavo Araújo (Distrito), Cristiano Leite de Castro (UFMG), Valéria Matarelli (Hermes Pardini), Kátia Torres (Linhagen), Paulo Lacativa (Biozeus), David Schlesinger (Mendelics), Miguel Mitne-Neto (Fleury), Mauro Teixeira (UFMG) and Lia Kubelka (Biogenetika).

[10] https://oglobo.globo.com/economia/negocios/noticia/2022/07/nao-dependemos-de-ter-uma-operadora-de-planos-de-saude-afirma-pedro-bueno-ceo-da-dasa-dona-de-alta-e-sergio-franco.ghtml, access on 26.09.2022.

[11] https://abstartups.com.br/, https://slinghub.io/, https://liga.ventures/, https://distrito.me/

[12] Inside HealthTech Report, Retrospectiva 2021 e Tendências 2022, available at https://materiais.distrito.me/mr/materiais-ricos-gratuitos.

[13] https://valor.globo.com/publicacoes/suplementos/noticia/2022/05/31/startup-que-monitora-o-paciente-atrai-investidor.ghtml, access on 26.09.2022.

[14] Mapeamento do ecossistema brasileiro de startups, 2021. ABStartups and Delloite.

[15] Inside HealthTech Report, Retrospectiva 2021 e Tendências 2022, available at https://materiais.distrito.me/mr/materiais-ricos-gratuitos.

[16] https://vesper-ventures.com/portfolio/

https://revistapegn.globo.com/Startups/noticia/2022/05/vesper-ventures-lanca-fundo-de-investimento-focado-em-startups-de-biotecnologia.html, access on 26.09.2022.

Please sign in or register for FREE

If you are a registered user on Research Communities by Springer Nature, please sign in