US Flood Governance Drives Social Inequity and Maybe the Next Housing Market Crash

Published in Social Sciences, Earth & Environment, and Sustainability

The US National Flood Insurance Program (NFIP), a public, federal program, was designed by Congress to be a safety net for flood-exposed homeowners after private insurers refused to take on the risk. From 1978 through 2004 the premiums collected from insured properties fully covered all claim payments to fix flood damages. But since 2004, losses made worse by rising sea levels and larger coastal storms have contributed to plunging the NFIP tens of billions of dollars into debt to the US Treasury, large chunks of which have periodically been paid off by the broader US tax base.

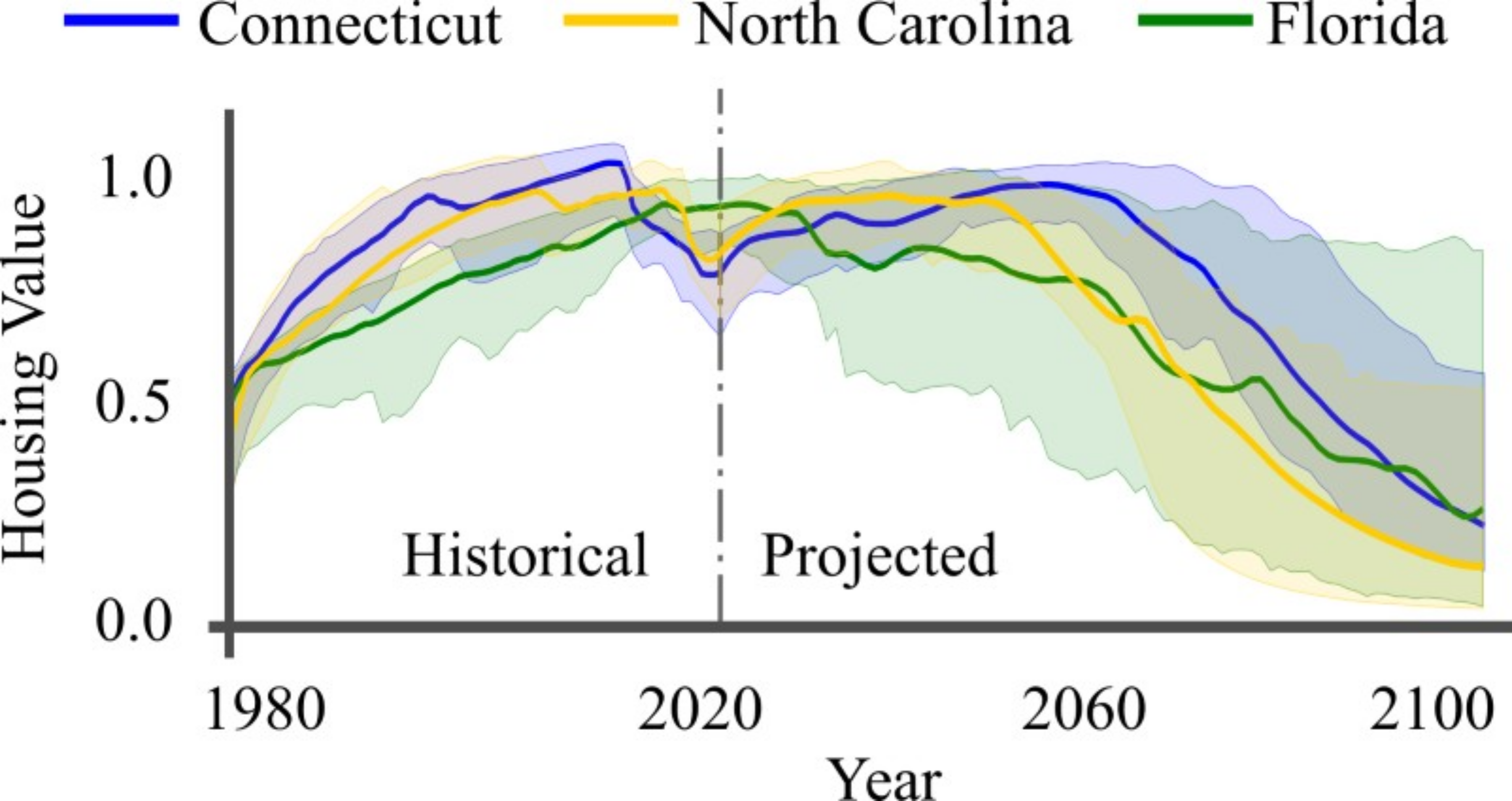

The fiscal and policy challenges facing the NFIP in recent years led us to wonder: what might the future of this program look like? Our socio-environmental forecasts, informed by climate projections, US census data, FEMA records, and Zillow home values, indicate that the business-as-usual approach to flood mitigation will cause the NFIP debt to increase further and culminate in a sudden housing market crash beginning sometime around 2060. Our research largely agrees with a 2016 report by Freddie Mac that forecasts 160 billion USD of the housing market will be under the high tide by 2050, and 238 billion by 2100.

These predictions may seem outrageous, but warning signs of a coming US coastal housing market crash are visible in 2024. Before Hurricane Sandy in 2012, coastal properties across the northeastern US were a sound investment, rising in value significantly faster than the national median. Since Sandy, northeastern coastal properties have been a less competitive investment, with home value growth lagging the national median by about 25%. In the months since hurricanes Helene and Milton, the US has paid 480 million USD to restore 54,000 damaged properties. Despite the NFIP-aided recovery of structures, market values have not recovered with listed sale prices dropping by approximately 15% at the time of this writing.

Our forecasts agree with what we’re seeing on the ground. Florida is likely to be the canary in the coal mine, showing a drop in coastal home values starting now. The mid-Atlantic and Gulf states will experience dramatic drops in home values starting around 2040. The northeastern US and west coast, naturally better shielded from intense coastal storms but not sea level rise, will follow in the decades after. Major parts of the coastal housing market that US taxpayers shore up through the NFIP will soon be lost to flood waters.

What is to be done? Maintaining the NFIP in its current form is likely the least desirable option for the US. Coastal storms will continue to pose serious risks to the health and safety of those in floodplains while stressing our emergency response agencies. Taxpayers are continuing to subsidize coastal real estate development, which principally benefits the better-off. Lower income coastal residents who are unable to afford a relocation on their own will watch as the accumulated wealth of a family-owned home is gradually eroded. Wealthy residents living at risk will continue to benefit financially from the NFIP until they decide to safely relocate.

Government-assisted, community-oriented relocations of coastal residents from flood-prone areas can address four of our problems at once. First, it might allow the US to sidestep a catastrophic housing market crash. Second, relocation would improve our national resilience to rising tides and coastal storms. Third, it would shield US taxpayers from the rising debt of the NFIP. Finally, approximately 70% of the land adjacent to the US shoreline is privately owned. Private coastlines can be converted into naturally restored public spaces, providing all residents with access to their nation's natural resources, while acting as a buffer from the storms and tides to come.

Follow the Topic

-

Communications Earth & Environment

An open access journal from Nature Portfolio that publishes high-quality research, reviews and commentary in the Earth, environmental and planetary sciences.

Introducing: Social Science Matters

Social Science Matters is a campaign from the team at Palgrave Macmillan that aims to increase the visibility and impact of the social sciences

Continue reading announcementRelated Collections

With Collections, you can get published faster and increase your visibility.

Hazards in Mountain Regions

Publishing Model: Open Access

Deadline: Nov 02, 2026

Ecosystems under marine heatwaves

Publishing Model: Hybrid

Deadline: Oct 22, 2026

Please sign in or register for FREE

If you are a registered user on Research Communities by Springer Nature, please sign in