Prospects, dynamics and dilemmas of agricultural insurance

Published in Sustainability

One drought away from sliding into absolute poverty — this is how Thomas Njeru, the co-founder of a micro-insurance firm in Kenya, describes the experience of small-scale farmers in the country. This fragile condition extends to other developing regions. Most of the world’s poorest people live in rural areas and depend directly on small-scale agriculture. In such contexts, weather-related disasters — likely to become more frequent and intense in the future — pose risks to human well-being, endanger food security, and discourage investment in productive technologies. Who dares to invest in expensive assets given the daunting possibility of losing everything to a storm? Needless to say, even if one considers investing, who will provide the financial means, given the associated risk? Developing mechanisms to cope with risk in small-scale agriculture is fundamental to alleviate chronic poverty and improve sustainability in developing countries.

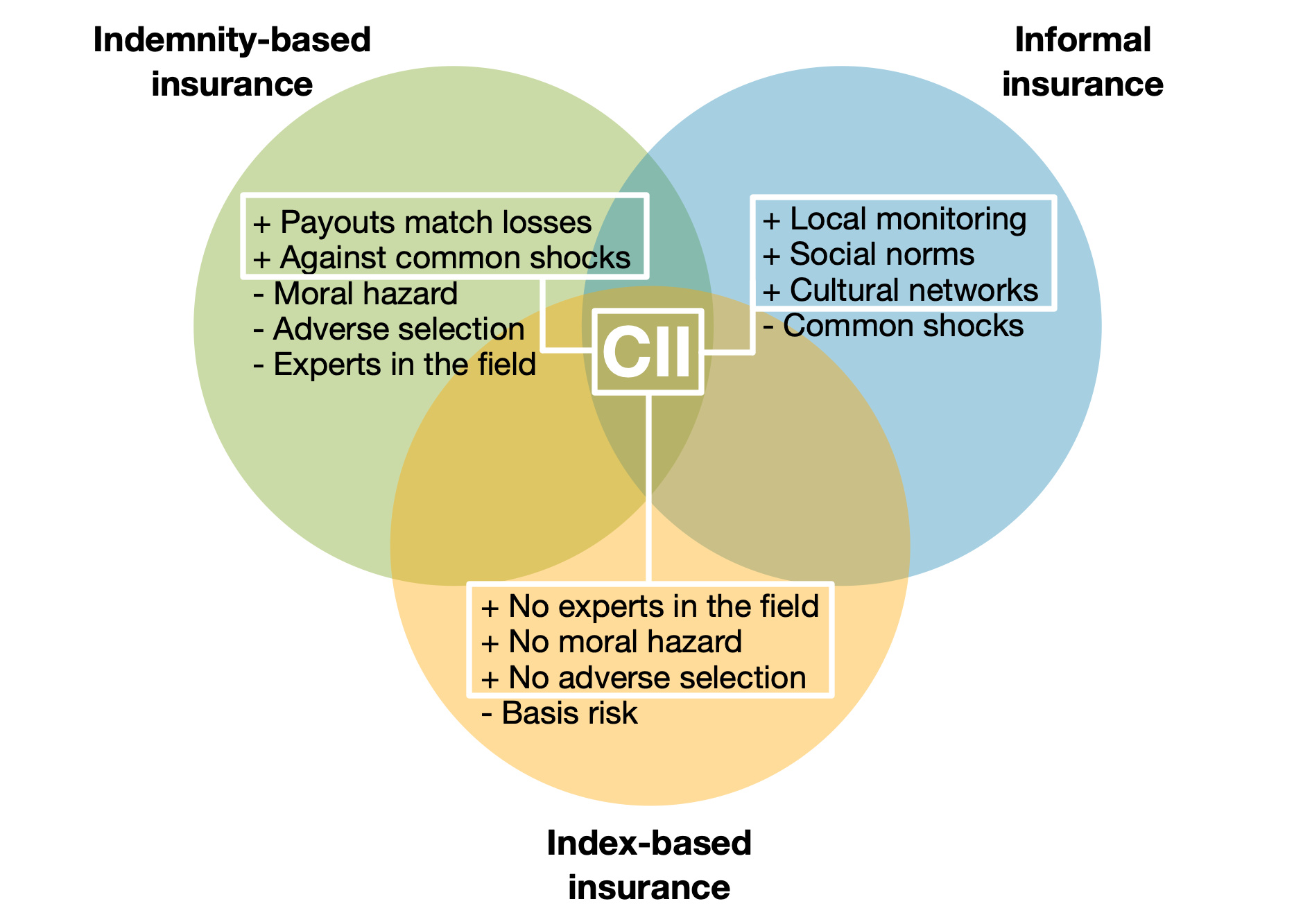

Insurance is one possible solution. Different types of insurance pose specific challenges. Over many generations, farmers developed informal insurance arrangements based on norms and reciprocity to safeguard neighbors’ isolated losses. While ingenious and often efficient, these arrangements will not protect farmers from catastrophes that affect whole communities simultaneously (so-called common shocks). The conventional alternative is to buy formal insurance from external organizations. Indemnity-based insurance allows farmers to receive compensations according to their losses, at the expense of paying a premium. These plans typically require experts in the field to evaluate damages, which may prove hard to deploy in developing countries, potentially increasing premium values. Indemnity-based insurance also suffers from adverse selection — only high-risk farmers subscribing — and moral hazard — negligence in reducing risk exposure. Index-based insurance constitutes yet another alternative. In this case, payments depend on objective weather indexes (for example, rainfall). While index-based insurance does not require experts in the field and mitigates moral hazard, new barriers are introduced: these plans suffer from basis risk — the possible mismatch between losses and triggering of the weather index. Moreover, people seem to have trouble understanding these insurance plans and fear incurring damages without receiving any compensation.

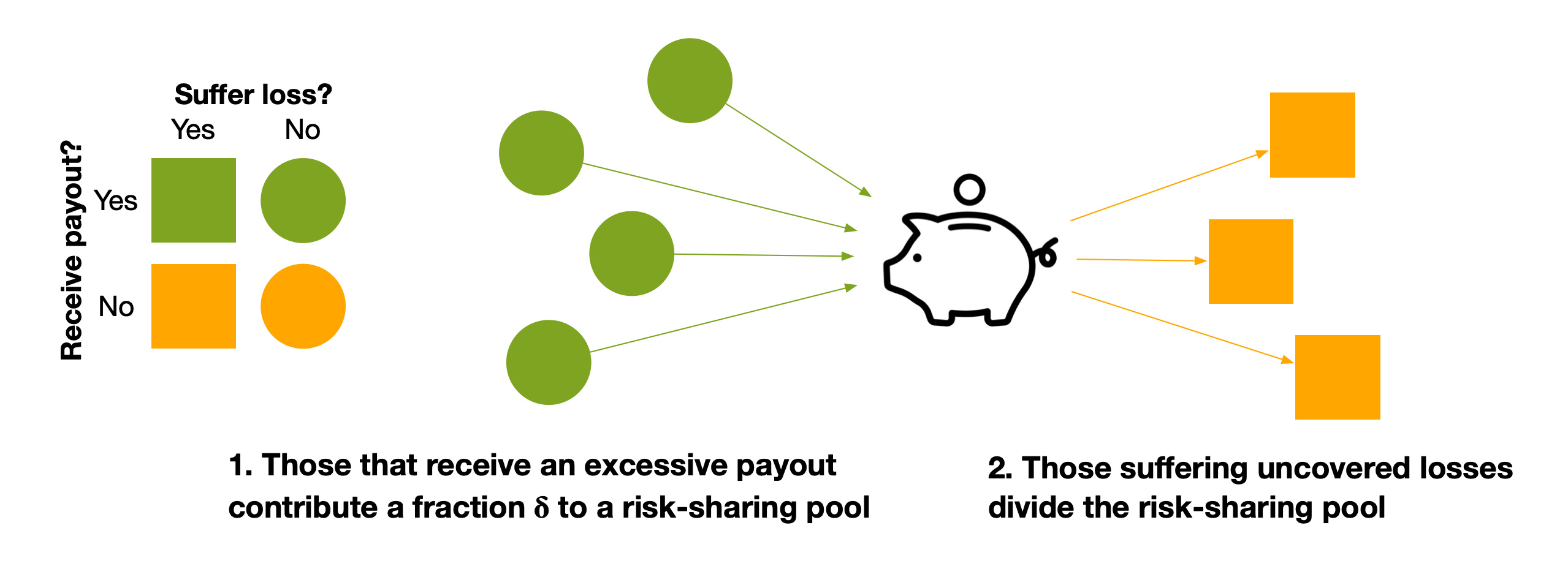

We analyze the dynamics of insurance adoption (using evolutionary game theory) when index-insurance is offered to collectives — called Collective Index Insurance (CII): groups of farmers receive payments based on a weather index; then, within groups, payouts are divided according to actual losses. Individuals that receive an excessive payout (that is, even without having losses) can contribute a fraction of that value to a risk-sharing pool that can benefit those that later suffer uncovered losses. The advantages of informal insurance (local monitoring), indemnity-based insurance (no basis risk) and index-based insurance (support even in case of common shocks) can be combined.

Collective index insurance plans can average out basis risk, yet they are no panacea. For insurance adoption to be stable, an initial critical mass of adopters is necessary; individuals must also monitor each other and guarantee that payouts are distributed fairly. Evolved norms of sharing may prove instrumental in this regard. Our work extends an invitation to harness well-established results on human prosociality to reason about mechanisms that may sustain cooperation among farmers. Is it possible to design collective insurance arrangements that are cheap, free of basis risk and stable? Yes. But it takes social norms, trust, local peer monitoring and prosociality. It takes a whole village!

Follow the Topic

-

Nature Sustainability

This journal publishes significant original research from a broad range of natural, social and engineering fields about sustainability, its policy dimensions and possible solutions.

What are SDG Topics?

An introduction to Sustainable Development Goals (SDGs) Topics and their role in highlighting sustainable development research.

Continue reading announcement

Please sign in or register for FREE

If you are a registered user on Research Communities by Springer Nature, please sign in